Smart Strategies for Purchasing Affordable Life Insurance introduction:

In today’s uncertain world, securing life insurance is not just a financial decision; it’s a strategic move to safeguard your loved ones’ future. However, with the plethora of options available, navigating through the intricacies of life insurance can be daunting. Moreover, the cost factor often becomes a deterrent for many individuals. But fear not, as we unveil smart strategies to purchase affordable life insurance without compromising on coverage or quality.

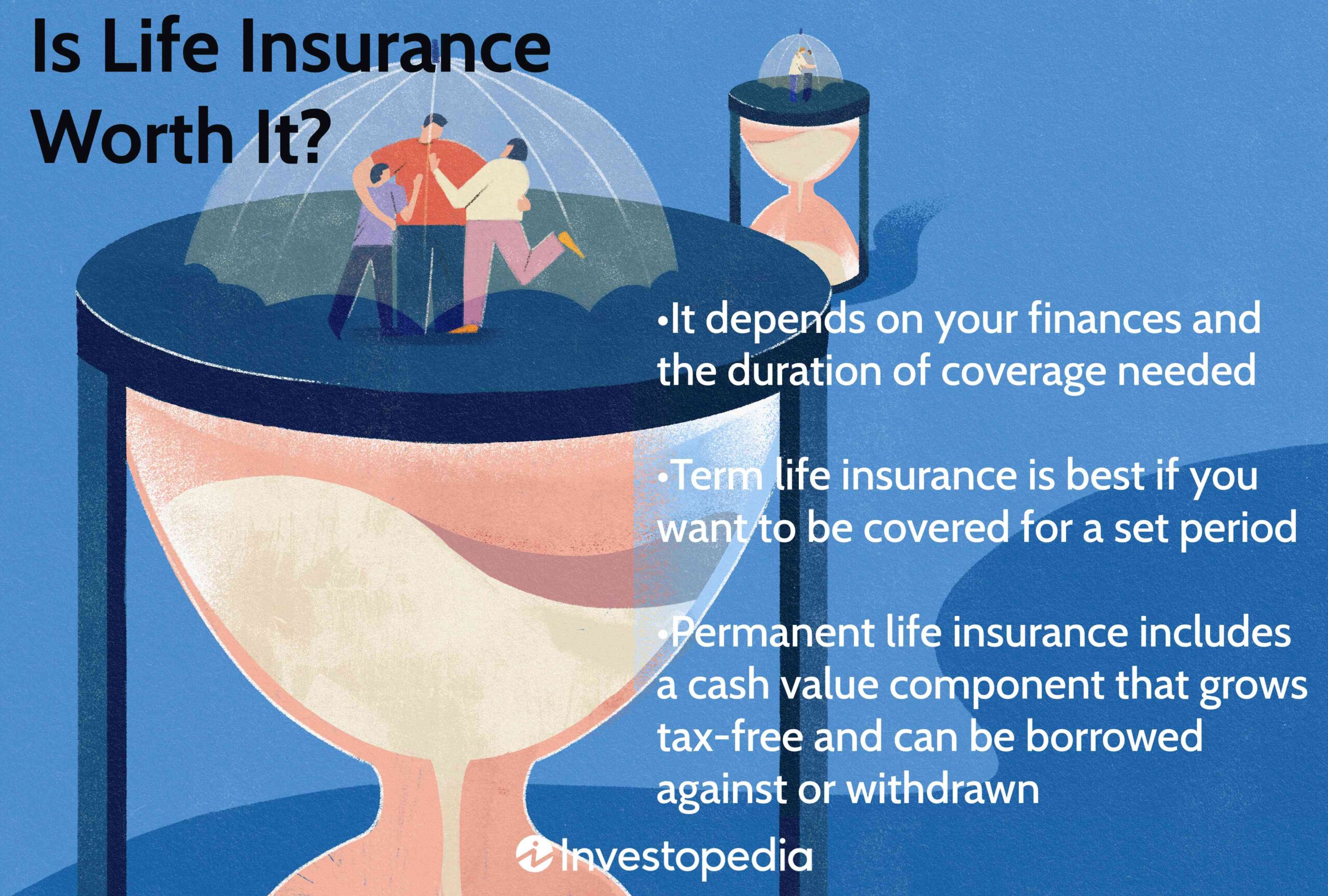

Understanding Your Needs

Before delving into the world of life insurance policies, it’s crucial to assess your needs comprehensively. Factors such as age, health condition, financial obligations, and long-term goals play a pivotal role in determining the type and extent of coverage required. Conducting a thorough evaluation of your current and future financial commitments will provide clarity on the appropriate coverage amount.

Term Life Insurance: A Cost-Effective Solution

For individuals seeking affordable life insurance with extensive coverage, term life insurance emerges as a compelling option. Unlike whole life or universal life policies, term life insurance offers coverage for a specified period, typically ranging from 10 to 30 years. Since it lacks cash value accumulation or investment components, term life insurance premiums are considerably lower, making it an ideal choice for budget-conscious individuals.

Embrace Health and Wellness

One of the most influential factors in determining life insurance premiums is your health status. Insurers often conduct medical examinations and scrutinize your medical history to assess the level of risk. Embracing a healthy lifestyle, which includes regular exercise, balanced diet, and routine medical check-ups, can significantly lower your premiums. Additionally, quitting smoking and reducing alcohol consumption can further decrease insurance costs, as tobacco and alcohol usage are associated with higher mortality rates.

Comparison Shopping: The Key to Savings

In the realm of life insurance, knowledge is power, and comparison shopping is the gateway to savings. With a myriad of insurance providers vying for your attention, investing time in researching and comparing policies can unearth substantial cost disparities. Online platforms and insurance aggregator websites facilitate side-by-side comparisons of premiums, coverage options, and rider benefits across multiple insurers. Leveraging these resources empowers you to make informed decisions and secure the most cost-effective life insurance policy tailored to your needs.

Optimize Coverage with Riders

Life insurance riders are supplementary benefits that can be added to your base policy to enhance coverage or provide additional protection. While some riders come at an extra cost, others may be included in certain policies or available at nominal premiums. Common riders include accelerated death benefit, which provides access to a portion of the death benefit in case of terminal illness, and waiver of premium rider, which waives premium payments if the policyholder becomes disabled. By strategically selecting riders that align with your needs, you can optimize coverage without significantly inflating costs.

Maintain a Healthy Credit Score

Surprisingly, your credit score can influence the cost of life insurance premiums. Insurers often consider creditworthiness as a predictive measure of financial responsibility and risk management. Individuals with higher credit scores are perceived as lower risk and may qualify for lower premiums. Therefore, maintaining a healthy credit score by managing debts responsibly, paying bills on time, and regularly monitoring your credit report can indirectly contribute to reducing life insurance costs.

Consider Group Insurance Options

For individuals seeking affordable life insurance coverage, group insurance plans offered through employers or professional associations present a viable alternative. Group insurance policies typically entail lower premiums compared to individual policies, as the risk is spread across a larger pool of participants. While group insurance may offer limited customization options and coverage may cease upon leaving the group, it serves as a cost-effective solution, especially for individuals with pre-existing health conditions or those seeking basic coverage.

Review and Reassess Periodically

Life is dynamic, and so are your insurance needs. As your circumstances change over time—whether it’s marriage, parenthood, career advancements, or retirement—it’s imperative to review and reassess your life insurance coverage periodically. Conducting a comprehensive review annually or upon significant life events enables you to adjust coverage levels, explore cost-saving opportunities, and ensure that your policy aligns with your evolving financial goals and priorities.

Conclusion

Securing affordable life insurance doesn’t have to be a daunting task. By adopting smart strategies such as understanding your needs, embracing health and wellness, comparison shopping, leveraging riders, maintaining a healthy credit score, considering group insurance options, and periodic review, you can navigate the complexities of life insurance with confidence. Remember, the goal is not just to find the cheapest policy, but to strike the optimal balance between affordability and comprehensive coverage to safeguard your loved ones’ future.